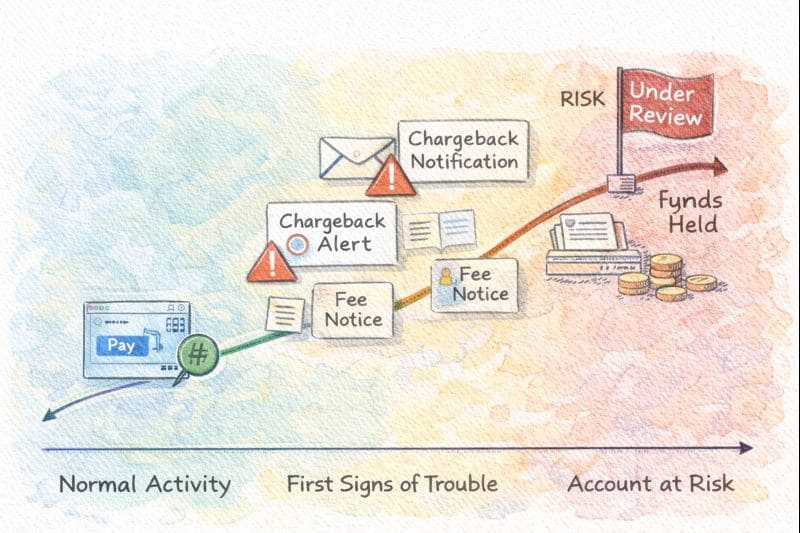

If you run an online business long enough, chargebacks stop feeling like a rare problem and start feeling like a silent leak. One or two turn into five. Five turn into warnings from your payment provider. Suddenly, funds are held, fees go up, and your merchant account is “under review.”

Most merchants don’t realize how serious chargebacks are until they’re already hurting cash flow and reputation. The good news? Chargebacks are not random. They follow patterns — and those patterns can be fixed.

This guide breaks down why chargebacks happen, how they damage your business, and what you can do to reduce them before they become a threat.

What a Chargeback Really Means for Your Business

A chargeback isn’t just a refund. It’s a dispute filed by a customer through their bank. When that happens:

- The sale amount is pulled from your account

- You’re charged an additional fee

- Your chargeback ratio increases

- Your merchant account risk profile worsens

Too many chargebacks can lead to higher processing fees, rolling reserves, or even account termination. For growing businesses, this is often the first major payment-related roadblock.

Why Chargebacks Keep Happening(The Real Reasons)

Most merchants assume chargebacks come from fraud alone. In reality, many are self-inflicted.

1. Unclear Billing Descriptors

Customers don’t recognize your business name on their statement. They assume fraud and dispute the charge.

2. Slow or Confusing Refunds

When customers can’t easily get a refund, they go straight to their bank.

3. Product or Service Mismatch

What the customer expected doesn’t match what they received — timing, quality, or delivery.

4. Fraudulent Transactions

Stolen cards still happen, especially for digital goods and international payments.

5. Poor Customer Communication

No response, delayed replies, or generic support emails push customers toward disputes.

How Chargebacks Slowly Destroy Merchant Accounts

Chargebacks don’t hurt all at once. They damage you quietly:

- Higher processing fees over time

- Funds placed on hold

- Increased scrutiny from banks

- Limited payment methods

- Difficulty switching providers later

Once your business is labeled “high risk,” recovery becomes much harder.

Practical Ways to Reduce Chargebacks (That Actually Work)

1: Use Clear Billing Descriptors

Make sure your business name, website, or support contact is visible on customer statements. Recognition alone prevents many disputes.

2: Tighten Your Refund Process

Fast, visible refunds reduce chargebacks dramatically. Make policies simple and easy to find — not hidden in fine print.

3: Set Customer Expectations Early

Clear product descriptions, delivery timelines, and terms reduce confusion. Ambiguity leads to disputes.

4: Add Basic Fraud Filters

Address verification, CVV checks, and IP monitoring catch obvious fraud without hurting conversions.

5: Keep Proof of Delivery and Usage

Digital receipts, login logs, shipping confirmations — these matter when disputes arise.

6: Respond to Chargebacks Quickly

Ignoring disputes almost guarantees a loss. Timely responses protect your ratios and reputation.

Why Payment Setup Matters More Than You Think

Your payment gateway and merchant account play a big role in chargeback control. The right setup provides:

- Early chargeback alerts

- Better reporting

- Dispute management tools

- Fraud prevention features

Merchants with the wrong payment partner often fight chargebacks blindly.

Turning Chargebacks Into a Wake-Up Call

Chargebacks aren’t just penalties — they’re feedback. Each dispute points to a gap in your checkout, communication, or delivery process.

Businesses that address these gaps early protect their revenue, reputation, and long-term growth.

Reducing chargebacks isn’t about eliminating every dispute. It’s about staying in control — before banks and processors take that control away.