Applying for a credit card merchant account is an important step for any business that wants to accept card payments without making any common merchant account approval mistakes. While many applications are approved without any , others are delayed or declined due to simple, avoidable Common Merchant Account Approval Mistakes.

Understanding these common merchant account approval mistakes can save time, reduce frustration, and improve your chances of getting approved on the first attempt.

Not Understanding How Merchant Accounts Work

One of the most common mistakes businesses make is applying without fully understanding how a merchant account works.

A merchant account is not just a formality. It plays a key role in:

- Holding card payment funds temporarily

- Managing refunds and chargebacks

- Reducing risk for banks and card networks

Businesses that misunderstand this process often submit unrealistic transaction estimates or incomplete information.

Before applying, it helps to understand what a credit card merchant account is and how it works, as approval decisions are based on this flow.

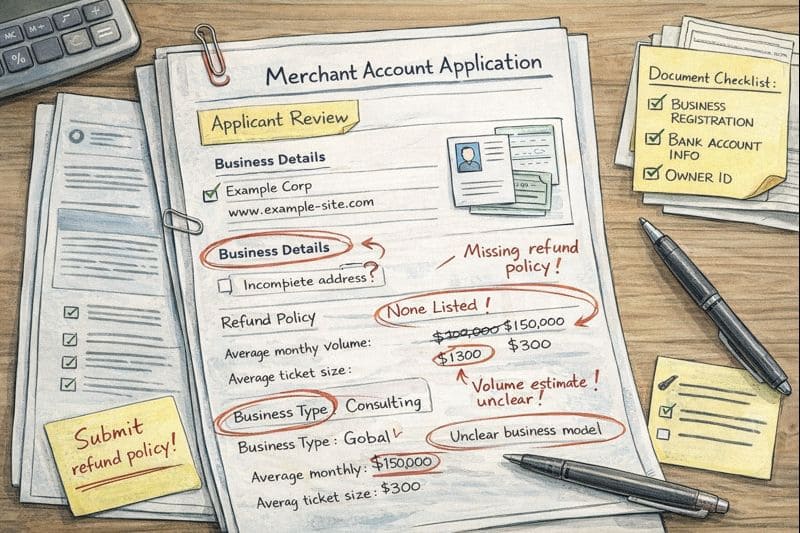

Incomplete or Inconsistent Business Information

Merchant account applications are detail-focused. Even small inconsistencies can cause delays.

Common issues include:

- Business name on the website not matching registration documents

- Different contact details across pages

- Missing ownership information

Payment providers rely on accuracy to assess legitimacy. Any mismatch raises questions during review.

Poor Website Transparency

A website review is a standard part of merchant account approval. Many applications fail simply because the website lacks clarity.

Common website-related mistakes:

- No clear description of products or services

- Missing refund or cancellation policy

- No contact page or business address

If you plan to accept credit card payments online, your website must clearly explain what customers are paying for and how issues are handled.

Unrealistic Transaction Estimates

Some businesses overestimate expected sales volume or underestimate refund rates, believing it improves approval chances. In reality, this often does the opposite.

Approval teams look for:

- Realistic average transaction values

- Reasonable monthly volume projections

- Honest customer location data

Unrealistic estimates suggest inexperience or risk.

Ignoring Industry Risk Factors

Certain industries receive more scrutiny than others. Failing to acknowledge this can hurt approval chances.

Examples include:

- Subscription-based services

- Digital products

- International sales

This doesn’t mean approval is impossible — it means applications must be well-prepared and transparent.

Weak Refund and Chargeback Policies

Refunds and chargebacks are a major concern for payment providers. Applications are often delayed when policies are unclear or missing.

Mistakes include:

- Vague refund terms

- No timeframe mentioned

- Policies hidden or difficult to find

Clear policies show responsibility and help reduce disputes later.

Applying Without Proper Documentation

Another common mistake is submitting an application without required documents ready.

These often include:

- Business registration documents

- Bank account details

- Identity verification for owners

Missing documents slow down the process and can lead to rejection.

Applying Too Early

If your site is unfinished or unclear, it’s often better to wait and apply once everything is in place. A well-prepared application usually leads to smoother approval.

Final Thoughts

Merchant account approval is not about speed or shortcuts. It’s about clarity, consistency, and preparation.

By avoiding these common mistakes and understanding how merchant accounts fit into the payment process, businesses can improve approval chances and build a more stable payment setup.