If you’ve ever opened your merchant account statement and felt confused while understanding merchant accout fees, you’re not alone.

Many business owners sign up for a merchant account expecting one simple fee, only to discover multiple charges appearing every month, some obvious, some hidden, and some never clearly explained. This lack of transparency is one of the biggest frustrations merchants face when accepting card payments.

In this guide, we’ll break down merchant account fees in plain language, explain why they exist, and show you how to avoid paying more than you should.

Why Merchant Account Fees Feel So Complicated

Most payment providers don’t clearly explain how their pricing works. Instead, merchants are given long agreements filled with technical terms, percentages, and conditions that are easy to overlook during signup.

Common complaints we hear from merchants include:

- “I was quoted one rate, but I’m paying much more.”

- “My fees change every month.”

- “I don’t understand why I’m being charged for declined transactions.”

- “There are fees even when I don’t process payments.”

The truth is, merchant account fees are made up of several different charges, not just one processing rate.

The Main Types of Merchant Account Fees

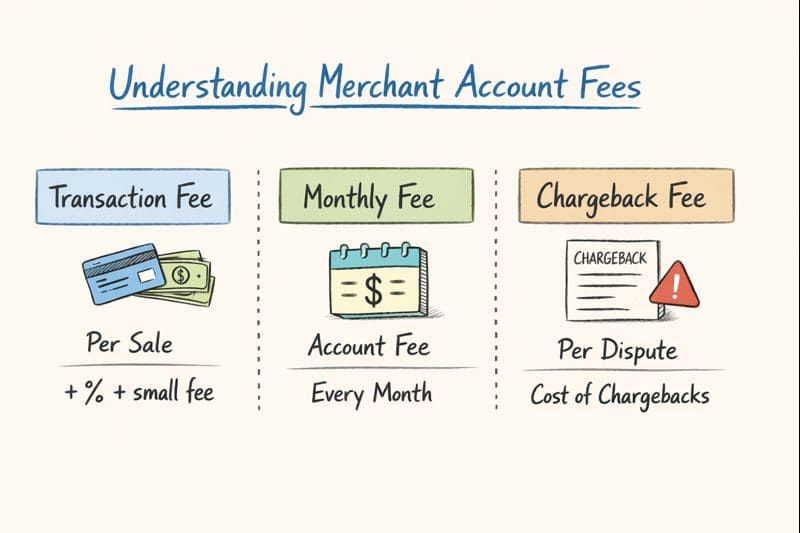

1. Transaction Fees

This is the fee charged every time a customer pays with a credit or debit card.

It usually includes:

- A percentage of the transaction amount

- A small flat fee per transaction

For example, you might pay a percentage plus a fixed amount for each successful Online payment processing. These fees exist because multiple parties are involved — banks, card networks, and processors.

Merchant pain point:

Small-ticket businesses feel these fees the most, as flat charges eat into profit.

Solution:

Choose a provider that offers fair pricing for your average transaction size, not just a low headline rate.

2. Monthly Fees

Some merchant accounts charge a monthly fee simply to keep the account active.

This may include:

- Account maintenance

- Access to reporting tools

- Customer support

Merchant pain point:

Paying monthly fees even during slow sales periods.

Solution:

Ask if monthly fees are negotiable or if there’s a minimum processing requirement instead.

3. Setup and Application Fees

Certain providers charge an upfront fee to open a merchant account. This may cover risk checks, underwriting, and account configuration.

Merchant pain point:

Paying upfront without guaranteed approval.

Solution:

Work with providers who clearly explain approval requirements before charging setup fees.

4. Chargeback Fees

When a customer disputes a transaction, a chargeback fee is applied — regardless of whether you win or lose the case.

These fees exist because disputes require manual review and bank involvement.

Merchant pain point:

Being charged even when fraud isn’t your fault.

Solution:

Use clear billing descriptors, proper customer support, and transaction records to reduce disputes before they happen.

5. Payment Gateway Fees

If you’re selling online, you’ll often pay a separate fee for the payment gateway — the technology that connects your website to the processor.

This fee may be:

- Monthly

- Per transaction

- Or both

Merchant pain point:

Unexpected extra fees beyond processing costs.

Solution:

Ask whether gateway fees are included or billed separately before signing up.

Why Your Fees Change Every Month

One of the most confusing aspects of high-risk merchant accounts is variable pricing.

Fees can change based on:

- Card type (credit vs debit)

- International cards

- Corporate or rewards cards

- Transaction volume

- Refunds and chargebacks

This is why two months with the same sales volume can still produce different fee totals.

How to Avoid Overpaying on Merchant Fees

Here are practical steps merchants can take to reduce unnecessary costs:

- Ask for a full fee breakdown in writing

Don’t rely on verbal promises. - Review statements monthly

Look for new or unexplained charges. - Understand your business risk level

High-risk businesses often pay more — but transparency still matters. - Avoid long-term contracts with heavy penalties

Flexibility protects you if fees become unreasonable. - Work with providers who explain, not hide

Good payment partners educate merchants instead of confusing them.

Choosing the Right Merchant Account Partner

A good merchant account provider doesn’t just process payments — they help your business grow without unnecessary financial strain.

When comparing providers, ask:

- Are fees clearly explained?

- Is support easy to reach?

- Do they understand my business model?

- Will my rates change without notice?

The right partner focuses on long-term relationships, not short-term profit from hidden fees.

Final Thoughts

Merchant account fees don’t have to be confusing.

When you understand how pricing works, you can make smarter decisions, avoid surprises, and keep more of your revenue where it belongs in your business.

The key is transparency, communication, and choosing a provider that treats merchants as partners, not numbers.