What are credit card processsing fees? Explained

If you accept credit card payments online, you already know one thing for sure — fees are unavoidable.

What most merchants don’t understand is why they are paying them, who is taking a cut, and whether those charges are actually fair.

Many business owners only start asking questions after they notice:

- Deposits that are lower than expected

- Monthly statements that are hard to read

- Fees that change without warning

- Conflicting explanations from processors

This confusion often leads to mistrust. Let’s clear that up.

Why Credit Card Processing Fees Exist

Every time a customer pays with a credit card, multiple systems work together to move money securely from the customer to your business.

These systems include:

- The card-issuing bank

- The card network (like Visa or MasterCard)

- The payment processor

- The payment gateway

- Your merchant account

Each party plays a role, and each one charges a small fee for that service.

The problem is not the fees themselves — it’s how poorly they are explained.

The Most Common Merchant Pain Point

Most merchants ask the same question:

“Why am I paying so many different fees for one transaction?”

The answer is simple: credit card processing fees are not one single charge, but a combination of several smaller ones.

Once you understand each part, your statement becomes much easier to read.

The Three Main Types of Credit Card Processing Fees

1. Interchange Fees (Paid to Banks)

Interchange fees are charged by the customer’s card-issuing bank. These fees cover:

- Credit risk

- Fraud protection

- Cardholder benefits

They vary based on:

- Card type (credit, debit, rewards)

- Transaction method (online vs in-person)

- Industry risk level

Important: Interchange fees are not set by your processor and cannot be negotiated.

2. Card Network Fees

Card networks charge small fees for routing transactions through their systems.

These fees are usually:

- A small percentage of the transaction

- A fixed per-transaction amount

Merchants rarely see these listed clearly, which adds to confusion.

3. Processor & Gateway Fees

This is where merchants often feel the most frustration.

These fees cover:

- Transaction handling

- Payment gateway usage

- Reporting tools

- Customer support

- Risk monitoring

Unlike interchange fees, processor fees vary widely between providers.

This is where smart merchants focus their negotiations.

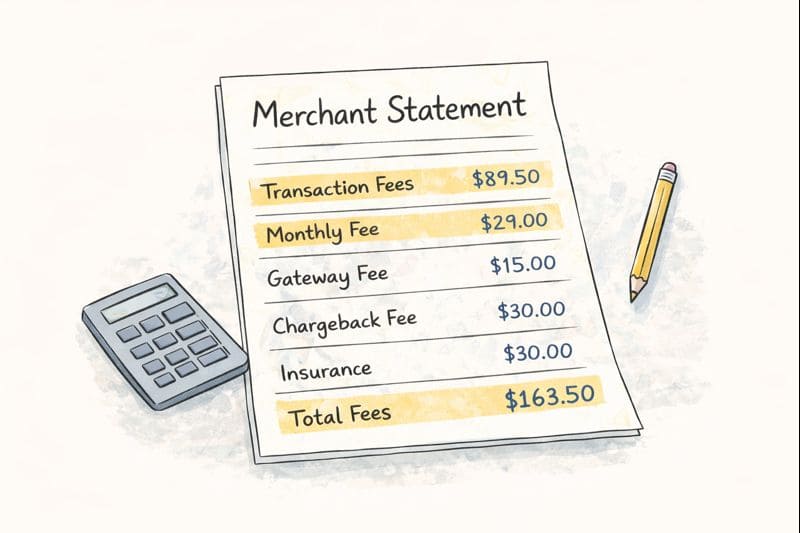

Common Fee Types Merchants See on Statements

If you’ve ever looked at your statement and felt overwhelmed, you’re not alone. Common line items include:

- Per-transaction fees

- Monthly account fees

- Gateway access fees

- Chargeback fees

- Refund processing fees

The issue is not that these fees exist — it’s that they are often not explained upfront.

Why Fees Feel Higher for Online Businesses

Online transactions carry more risk than in-person payments. Since the card isn’t physically present, banks and networks add extra safeguards.

This often results in:

- Slightly higher interchange rates

- Stricter fraud checks

- More frequent declines

Merchant concern: “I’m losing money just to accept payments.”

Reality: You’re paying for security, infrastructure, and global reach — but that doesn’t mean you should overpay.

How to Reduce Credit Card Processing Costs Without Cutting Corners

Here are practical steps merchants can take:

1. Understand Your Pricing Model

Know whether you’re on:

- Flat-rate pricing

- Tiered pricing

- Interchange-plus pricing

Transparency matters more than the lowest advertised rate.

2. Reduce Chargebacks and Refunds

Chargebacks increase processing costs and can raise your risk profile.

Clear billing descriptors and customer communication help more than most merchants realize.

3. Use Smart Fraud Tools

Better fraud filtering reduces false declines and unnecessary losses.

4. Ask Questions Before Signing

If a provider cannot clearly explain their fees, that’s a warning sign.

The Real Cost of “Cheap” Processing

Some merchants chase the lowest rates and end up paying more through:

- Hidden fees

- Poor support

- Payment failures

- Account freezes

Reliable processing with clear pricing often costs less in the long run.

Final Thoughts

Credit card processing fees don’t have to be mysterious or intimidating.

Once you understand:

- Who charges what

- Why those fees exist

- Where you can and can’t negotiate

You gain control over your payment setup.

Payments should support your business — not create stress. And the right understanding makes all the difference.