One of the most common questions online merchants ask after starting to accept card payments is:

“The payment was approved, so why haven’t I received the money yet?”

This confusion usually comes from not understanding the difference between authorization vs settlement in card payment.

They sound similar, they happen close together, but they serve very different purposes. Once you understand the gap between the two, many payment-related frustrations suddenly make sense.

The Problem Merchants Commonly Face With Authorization vs Settlement in Card Payments

Merchants often encounter situations like:

- A customer’s payment shows as “approved,” but no funds arrive

- Transactions appear in reports but not in the bank

- Customers see charges pending for days

- Orders ship before payments are fully completed

This leads to uncertainty, cash flow stress, and sometimes costly mistakes.

The root of the issue is misunderstanding authorization vs settlement.

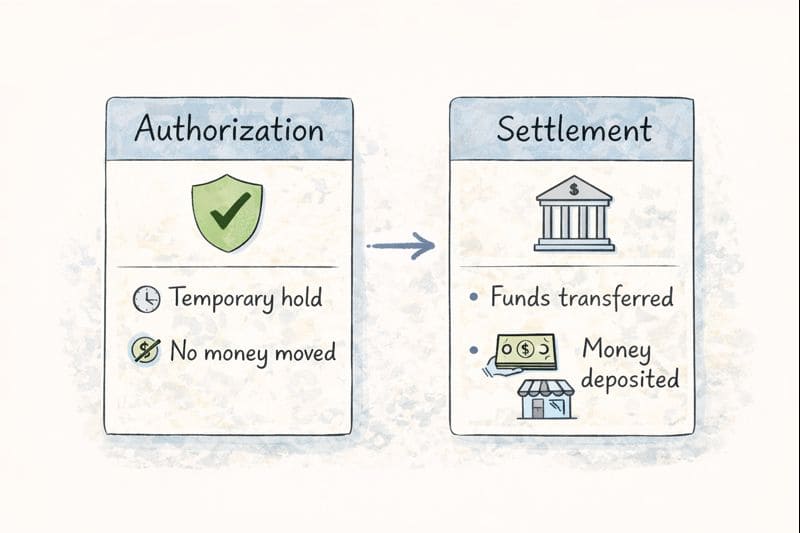

What Is Authorization?

Authorization is the first step in a card payment.

When a customer places an order and enters their card details, the issuing bank checks:

- Is the card valid?

- Are sufficient funds available?

- Does the transaction look legitimate?

If everything checks out, the bank sends back an authorization approval.

What Authorization Means for Merchants

- The funds are reserved, not transferred

- The payment is not final yet

- The money is still with the customer’s bank

Important: Authorization only confirms that the customer can pay — not that you’ve been paid.

Common Problems With Authorization

“The payment was approved, so I shipped the order — now the payment failed later.”

This happens when merchants treat authorization as completed payment.

Solution: Always understand that authorization is temporary and depends on proper settlement afterward.

What Is Settlement?

Settlement is the step where the authorized transaction is completed, and funds are moved from the customer’s bank to your merchant account.

This usually happens when:

- Transactions are batched

- Sent for clearing

- Processed by the card networks

- Deposited into your merchant account

Settlement typically takes one to several business days, depending on your processor and bank.

Why Authorization and Settlement Are Separate

Card payment systems are designed this way to:

- Reduce fraud

- Allow corrections before funds move

- Handle refunds and reversals more easily

This separation protects both merchants and customers — but only if merchants understand it.

What Happens If Settlement Doesn’t Occur?

Incase the authorized transaction is not settled in time:

- The authorization expires

- The reserved funds are released back to the customer

- The merchant receives nothing

This often happens when:

- Orders are delayed

- Batches are not closed properly

- System errors occur

Merchant pain point: “I thought I got paid, but the money disappeared.”

Solution: Ensure transactions are settled promptly and systems are configured correctly.

Authorization Holds and Customer Confusion

Customers sometimes see:

- Pending charges

- Duplicate-looking transactions

- Temporary holds on their card

This can lead to complaints and refund requests.

Merchant best practice: Clearly explain pending charges in confirmation emails or support responses to reduce disputes.

How Authorization and Settlement Affect Cash Flow

Understanding this timing helps merchants:

- Plan payouts realistically

- Avoid overspending expected funds

- Manage inventory and shipping wisely

Merchants who rely on authorization alone often face cash flow gaps they didn’t anticipate.

How to Reduce Issues Between Authorization and Settlement

Here are practical steps merchants can take:

1. Set Clear Order Processing Rules

Ship orders only after settlement or when you’re confident settlement will occur.

2. Monitor Your Payment Reports

Regularly review authorized vs settled transactions to catch issues early.

3. Use Reliable Payment Partners

Choose processors and gateways known for stable settlement cycles and transparent reporting.

4. Communicate with Customers

Clear communication reduces confusion and unnecessary disputes.

Why This Knowledge Matters

Merchants who understand authorization vs settlement:

- Avoid shipping without payment

- Reduce payment-related stress

- Improve customer trust

- Gain better control over cash flow

Payments become predictable instead of frustrating.

Final Thoughts

Authorization and settlement are two sides of the same transaction — but they are not the same thing.

Authorization confirms a customer’s ability to pay.

Settlement is when you actually receive the money.

Once you understand this difference, many payment mysteries disappear, and your business runs with greater confidence and clarity.