As your business grows and your merchant account handles more transactions, two things become inevitable: refunds and chargebacks. While many merchants dread these, understanding how they work and managing them effectively can save your business from unnecessary losses and stress.

Refunds and chargebacks aren’t just accounting tasks — they directly affect your cash flow, fees, and even your standing with your merchant account provider. Let’s break down what they are, why they happen, and how to handle them.

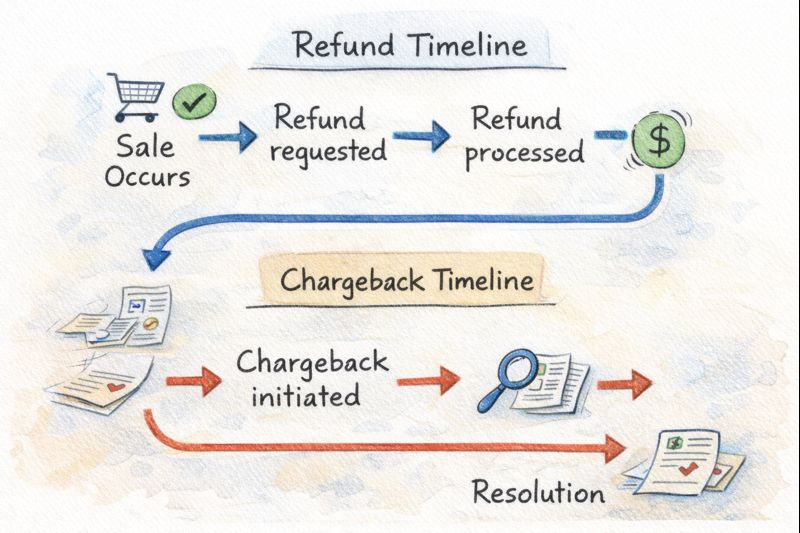

What Is a Refund?

A refund happens when a customer requests their money back after a completed transaction. It could be for reasons like:

- Product dissatisfaction

- Wrong item shipped

- Duplicate payment

Refunds are generally straightforward. Most merchant accounts allow you to issue them directly through your payment gateway. However, repeated refunds can signal risk to your provider and may affect your credit card processing fees.

Merchant pain point:

“Refunds reduce my available funds and sometimes take several days to reflect in my bank account.”

Solution:

Track refunds carefully and set internal policies to minimize errors. Always communicate clearly with the customer to avoid disputes escalating into chargebacks.

What Is a Chargeback?

A chargeback occurs when a customer disputes a transaction with their bank. Reasons may include:

- Unauthorized or fraudulent transactions

- Product not delivered

- Misrepresentation of product or service

Unlike refunds, chargebacks are initiated by the customer’s bank, not the merchant. They can take longer to resolve, often holding funds in reserve during the investigation.

Merchant pain point:

“Chargebacks freeze my money and can lead to higher fees or account reviews.”

Solution:

Maintain clear documentation of transactions, shipping, and communications. Use tracking numbers, receipts, and proof of delivery to defend against disputes.

Why Refunds and Chargebacks Affect Your Merchant Account

Refunds and chargebacks don’t just remove money from your account. They can also:

- Increase processing fees

- Trigger rolling reserves or holds

- Affect your merchant account’s risk rating

- Lead to account termination if excessive

Even a small business with good sales can suffer if chargebacks aren’t managed proactively.

How to Managing Refunds and Chargebacks

Tips for Refund Management Effectively

- Create a Clear Refund Policy

Publish an easy-to-find, simple policy to set expectations. Clear rules reduce disputes and improve customer trust. - Automate Refund Processing

Use your payment gateway tools to process refunds quickly, ensuring customers get money back promptly and reducing friction. - Track Refunds Against Sales

Monitor refund trends to spot recurring issues like defective products or frequent errors in order fulfillment.

Tips for Minimizing Merchant Account Chargebacks

- Provide Accurate Descriptions

Misunderstandings about the product or service are a major cause of disputes. Accurate listings reduce risk. - Maintain Proof of Delivery

Shipping confirmation, tracking numbers, and signed receipts help win disputes. - Communicate Promptly

Respond quickly to complaints and attempt resolution before the customer contacts their bank. - Monitor High-Risk Transactions

Large orders, international payments, or first-time customers require extra verification to prevent fraud.

Leveraging Your Merchant Account Tools

Modern merchant accounts and payment gateways include features to help manage refunds and chargebacks:

- Automatic dispute notifications

- Reporting dashboards

- Risk management alerts

Using these tools proactively can save time, prevent losses, and maintain your account’s good standing.

Final Thoughts

Refunds and chargebacks are part of doing business. They aren’t inherently bad — but unmanaging payment gateway disputes, they can hurt your cash flow, raise fees, and put your merchant account at risk.

By understanding the difference between refunds and chargebacks, keeping accurate records, and using merchant account tools wisely, businesses can minimize losses and maintain a healthy relationship with customers and their payment provider.

Pro tip: Review your merchant account agreements periodically to ensure your refund and transaction disputes management practices align with provider policies. Staying proactive now prevents major headaches later.