If you’re planning to accept credit card payments on your website, you’ve likely come across two common terms: payment gateway and merchant account. Many businesses assume they are the same thing, but they serve very different purposes.

Understanding the difference between a payment gateway and a merchant account is important before setting up online payments. Choosing the wrong setup can lead to processing delays, higher fees, or failed transactions.

This guide explains what each one does, how they work together, and why most online businesses need both.

What Is a Payment Gateway?

A payment gateway for online business is the technology that securely transfers payment information from your website to the bank or payment processor.

When a customer enters their credit card details during checkout, the payment gateway:

- Encrypts the card information

- Sends it for authorization

- Confirms whether the transaction is approved or declined

In simple terms, the payment gateway acts as the bridge between your website and the payment processor.

Payment gateways can be:

- Hosted (redirecting customers to another page)

- Integrated (embedded directly into your checkout)

What Is a Merchant Account?

A merchant account is a special bank account that allows businesses to receive credit card payments. It temporarily holds the funds from approved transactions before they are transferred to your regular business bank account.

A merchant account is required because credit card payments cannot be deposited directly into a standard bank account.

Key functions of a merchant account include:

- Receiving card payment funds

- Holding funds during settlement

- Managing refunds and chargebacks

Without a merchant account, credit card payments cannot be processed properly.

Before applying for a credit card merchant account, businesses should understand how funds are settled and held.

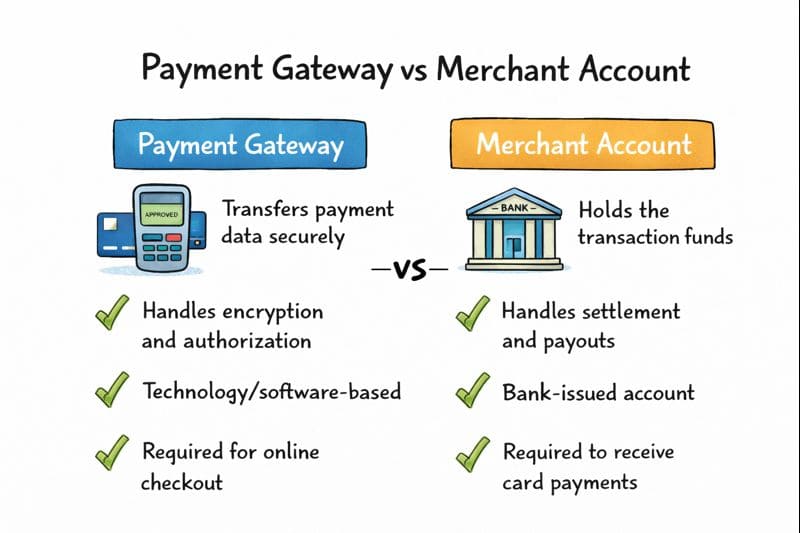

Payment Gateway vs Merchant Account: The Core Difference

Although they work closely together, their roles are very different.

| Payment Gateway | Merchant Account |

| Transfers payment data securely | Holds the transaction funds |

| Handles encryption and authorization | Handles settlement and payouts |

| Technology/software-based | Bank-issued account |

| Required for online checkout | Required to receive card payments |

Think of it this way:

- The payment gateway moves the information

- The merchant account moves the money

Do You Need Both?

In most cases, yes.

To accept credit card payments online, businesses usually need:

- A payment gateway to securely process the transaction

- A merchant account to receive and settle the funds

Some providers offer both together, while others provide them separately. Understanding the difference helps you choose the setup that best fits your business.

How They Work Together in an Online Payment

Here’s a simplified flow of what happens during a transaction:

- Customer enters card details on your website

- Payment gateway encrypts and sends the data

- Transaction is authorized

- Funds are placed in the merchant account

- Funds are settled to your business bank account

Each step depends on both components working correctly.

Common Mistakes Businesses Make

Many businesses run into issues because they misunderstand these roles. Common mistakes include:

- Assuming a payment gateway alone is enough

- Not understanding settlement timelines

- Choosing a setup that doesn’t support international cards

- Overlooking chargeback management

Knowing the difference early can prevent setup delays and unexpected problems later.

Choosing the Right Setup for Your Business

When deciding on a payment gateway and merchant account, consider:

- Your business type and risk level

- Expected transaction volume

- Local or international customers

- Settlement speed and fees

The right combination will allow you to accept credit card payments online smoothly while maintaining control over transactions.

Final Thoughts

A payment gateway and a merchant account are not interchangeable — they are two essential parts of online payment processing. One handles the secure transfer of data, while the other handles the movement of funds.

Understanding how they work together helps businesses make informed decisions, avoid technical issues, and create a reliable payment experience for customers.