As online businesses grow, one question comes up again and again:

Should you rely on card payments, or is direct debit the better option?

Both payment methods move money from customers to businesses. But how they work, how they fail, and how they affect cash flow are very different. Choosing the wrong one can quietly cost you revenue, customers, and time.

This guide breaks down the real differences — without technical language — so you can decide what fits your business model best.

The Core Problem Merchants Are Trying to Solve

Most businesses aren’t looking for “more payment methods.”

They’re trying to fix problems like:

- Late or missed payments

- High transaction fees

- Payment failures and declines

- Chargebacks and disputes

- Unpredictable cash flow

Direct debit and card payments solve different versions of these problems.

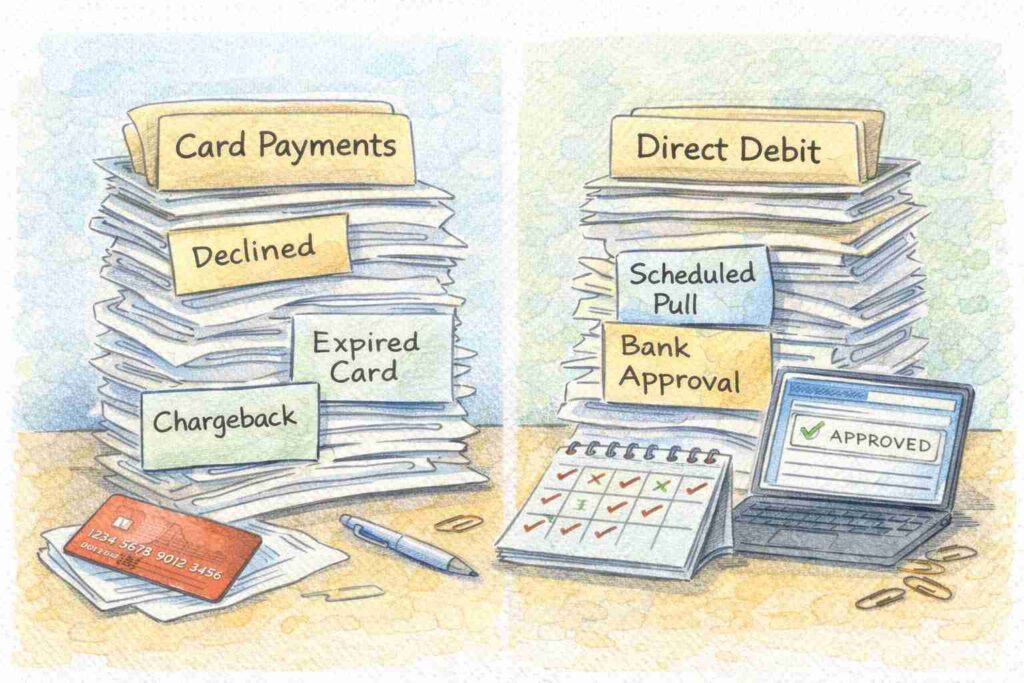

How Card Payments Work (From a Merchant’s View)

Card payments are instant, familiar, and flexible. Customers enter their card details, the transaction is approved, and funds move through the payment gateway and banks.

Why Merchants Like Card Payments

- Fast authorization

- Works well for one-time purchases

- Familiar checkout experience

- Easy to scale internationally

Where Card Payments Cause Pain

- Card expirations and declines

- Higher processing fees

- Chargebacks and fraud disputes

- Failed recurring payments

For businesses with subscriptions or repeat billing, these issues add up fast.

How Direct Debit Works (In Simple Terms)

Direct debit allows a business to pull funds directly from a customer’s bank account — with permission — on a scheduled basis.

Instead of asking customers to “pay now” every time, payments happen automatically.

Why Businesses Choose Direct Debit

- Lower transaction fees

- Fewer failed payments

- No card expiration issues

- Predictable billing cycles

Where Direct Debit Has Limits

- Slower setup process

- Not ideal for impulse purchases

- Requires customer trust

- Less flexible for one-off sales

Direct debit shines in stability, not speed.

Side-by-Side: What Really Matters to Merchants

Cash Flow

- Card payments: Immediate but inconsistent

- Direct debit: Predictable and stable

Payment Failures

- Card payments: Common (expired cards, limits, fraud blocks)

- Direct debit: Much lower failure rates

Chargebacks & Disputes

- Card payments: High exposure

- Direct debit: Fewer disputes, clearer reversal process

Customer Experience

- Card payments: Familiar and fast

- Direct debit: Convenient for long-term relationships

Which Businesses Benefit Most from Card Payments?

Card payments work best for:

- E-commerce stores

- One-time purchases

- International customers

- Digital products and instant delivery

If speed and flexibility matter more than long-term predictability, cards make sense.

Which Businesses Benefit Most from Direct Debit?

Direct debit is ideal for:

- Subscription services

- SaaS platforms

- Memberships

- Utilities and recurring billing

If stable revenue and low churn matter more than instant checkout, direct debit wins.

The Smart Approach: Use Both Strategically

Many growing businesses don’t choose one — they combine both.

- Card payments for sign-ups and one-time sales

- Direct debit for renewals and recurring billing

This reduces declines, lowers fees, and smooths cash flow over time.

Final Thoughts

There’s no universal “better” payment method — only what fits your business model.

Card payments bring speed and reach.

Direct debit brings stability and control.

The best choice is the one that reduces friction for your customers and risk for your business.

Understanding this difference early helps you build a payment setup that supports growth instead of slowing it down.