If your business is selling online, it’s likely that at some point you’ve wondered:

“How do I accept credit card payments from customers in other countries?”

International credit card payments may sound simple — the customer enters a card, you get paid — but in reality, they involve a few extra steps and considerations. Without understanding them, merchants often face:

- Declined international transactions

- Unexpected fees

- Currency conversion issues

- Customer disputes or chargebacks

Let’s break it down in a way that helps you accept international payments confidently and avoid common pitfalls.

Why International Payments Can Be Tricky

Domestic transactions are straightforward: your payment processor, card network, and bank all operate in the same country. International payments, however, add extra layers:

- Currency conversion – paying and receiving in different currencies

- Cross-border fees – banks and networks may charge additional percentages

- Different card networks – some cards are widely accepted internationally, others are not

- Fraud checks – foreign transactions are often flagged for security

Many merchants struggle simply because they aren’t aware of these factors upfront.

How International Credit Card Payments Work

The steps are similar to domestic payments, with a few key differences:

1. Customer Makes a Purchase

The buyer enters their card details at checkout. Their card may be in a foreign currency.

Merchant pain point: “Why does the customer’s bank sometimes decline a perfectly valid card?”

Solution: Some banks restrict foreign transactions or require extra authentication.

2. Payment Gateway and Processor Handle the Transaction

Your payment gateway sends the payment request to your processor, which contacts the customer’s card network.

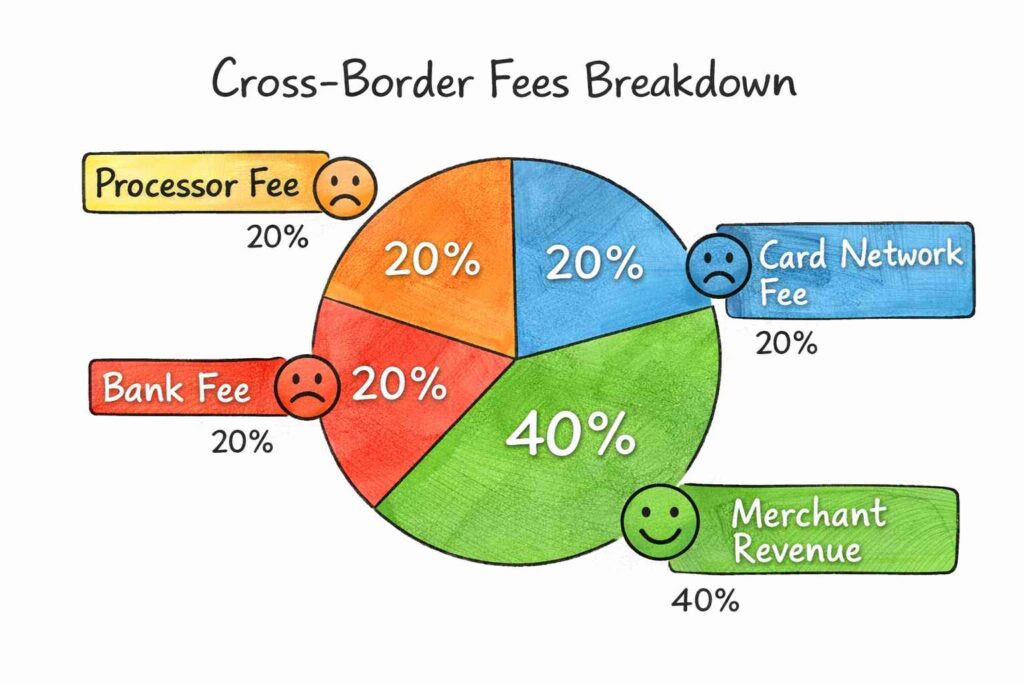

- Cross-border fees and currency conversion are calculated here.

- Some processors automatically convert the amount to your preferred currency.

3. Card Network Authorization

The card network communicates with the issuing bank. The bank checks:

- Card validity

- Available funds

- Transaction legitimacy

Problem: International payments are more likely to be declined due to fraud rules.

Solution: Use a payment processor experienced in international payments and ensure your merchant account is enabled for cross-border transactions.

4. Settlement and Currency Conversion

Once approved, the transaction is settled:

- Funds are deposited into your merchant account

- Currency conversion is applied if needed

- Cross-border fees are deducted

Merchant pain point: “Why did I receive less than expected?”

Solution: Understand your processor’s fees for international payments and factor them into pricing.

Common Issues Merchants Face

- Unexpected Cross-Border Fees: Banks and card networks may charge a small percentage on top of the standard processing fee.

Tip: Compare international fee rates among processors before choosing one.

- Higher Fraud Risk: Fraud checks are stricter for international transactions. Cards may be declined or require verification.

Tip: Enable 3D Secure or similar fraud protection features.

- Currency Conversion Confusion: The customer may be charged in their currency, but your account receives a different amount after conversion.

Tip: Clearly display currency conversion at checkout to reduce disputes.

How to Accept International Payments Smoothly

- Choose the right processor: Ensure it handles cross-border payments efficiently.

- Enable multiple currencies: Let customers pay in their preferred currency.

- Transparent pricing: Clearly communicate fees to avoid surprises.

- Fraud management: Use verification tools to reduce declines and chargebacks.

- Check card types: Know which international cards are widely accepted in your target markets.

Why International Payments Are Worth It

Despite the extra steps, accepting international credit cards opens your business to global customers, increases sales, and boosts credibility.

The key is preparation: understand the process, anticipate common problems, and partner with a processor that supports your international ambitions.

Final Thoughts

International credit card payments don’t have to be confusing or risky. By understanding the process, fees, and potential challenges, merchants can:

- Accept payments confidently

- Avoid costly surprises

- Expand globally without unnecessary friction

Your online business can thrive internationally — it’s just a matter of knowing what happens behind the scenes and planning accordingly.