Selling products or services internationally is exciting — but accepting credit card payments from customers in other countries can be confusing.

Many merchants face these challenges:

- Payments declined without clear reason

- Unexpected fees eating into revenue

- Delays due to currency conversion or bank processing

- Increased risk of chargebacks

Understanding how cross-border credit card payments actually work can help merchants avoid mistakes, optimize fees, and expand globally with confidence.

What Is a Cross-Border Credit Card Payment?

A cross-border payment occurs when a customer’s card is issued in a different country than the merchant’s bank account.

Unlike domestic payments, cross-border transactions often involve:

- Currency conversion

- Additional network and bank fees

- Extra fraud and compliance checks

Merchants who ignore these factors often see higher declines, unhappy customers, and revenue losses.

Step-by-Step: How Cross-Border Payments Work

1. Customer Enters Payment Information

The buyer selects their items, enters card details, and clicks “Pay Now.”

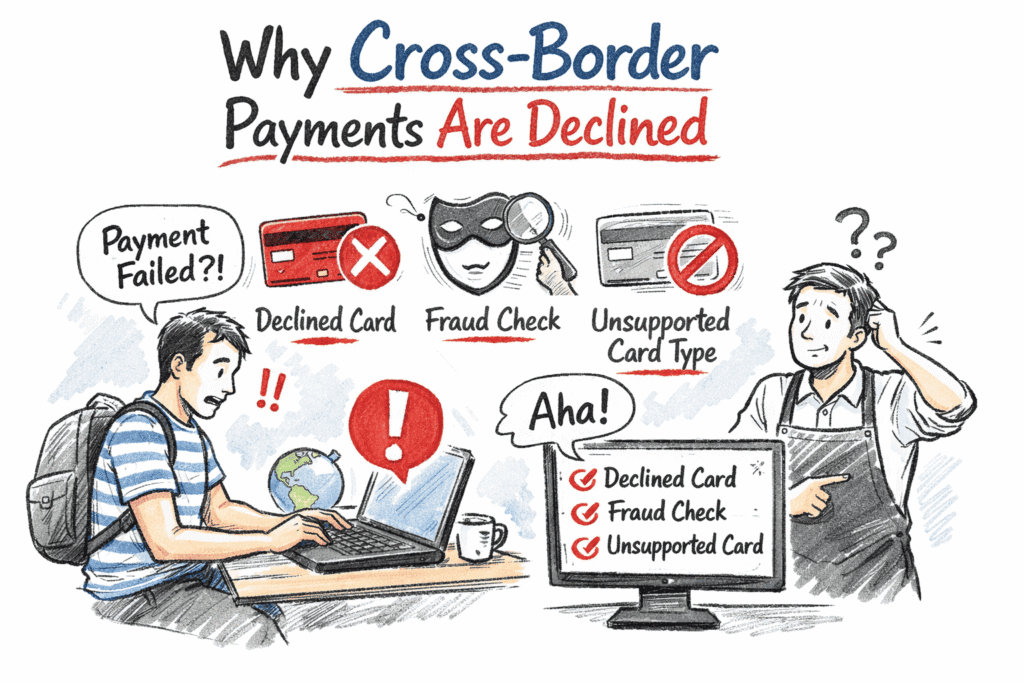

Merchant pain point: “Why was the card declined?”

Solution: Banks may restrict international transactions or flag foreign payments for verification.

2. Payment Gateway Secures the Transaction

The payment gateway encrypts card details and forwards the transaction to the processor.

- Ensures PCI compliance

- Protects merchant and customer data

- Routes the payment to the card network

3. Processor and Card Network Handle the Payment

The processor communicates with the card network (Visa, Mastercard, Amex) to reach the customer’s issuing bank.

- Determines applicable cross-border fees

- Initiates currency conversion if needed

Merchant pain point: “Why do I get less than the purchase price?”

Solution: Understand processor fees and exchange rates for cross-border transactions.

4. Issuing Bank Authorizes or Declines

The customer’s bank checks:

- Card validity

- Available funds

- Fraud and security rules

Foreign cards are more likely to be declined because of strict fraud rules, unusual purchase locations, or currency restrictions.

Tip for merchants: Enable 3D Secure or additional verification to reduce declines.

5. Settlement and Fund Transfer

Once approved, the transaction is settled:

- Money moves from the customer’s bank → processor → merchant’s acquiring bank

- Cross-border and currency conversion fees are applied

- Funds appear in the merchant account, typically a few days later

Merchant pain point: “I see a delay in receiving funds.”

Solution: Inform customers of potential processing time; choose a processor experienced with international payments.

Common Challenges Merchants Face

- High Cross-Border Fees

These include processor, network, and bank fees.

Fix: Compare providers and factor fees into pricing.

- Currency Conversion Fluctuations

Exchange rates may reduce your revenue.

Fix: Offer multi-currency checkout or monitor conversion rates.

- Payment Declines

Foreign cards are more frequently declined.

Fix: Use fraud filters smartly and ensure your merchant account allows international cards.

- Chargebacks and Disputes

International customers may dispute transactions for unfamiliar charges.

Fix: Provide clear invoices and currency transparency.

Best Practices for Smooth Cross-Border Payments

- Enable multiple currencies: Let customers pay in their preferred currency.

- Use a global payment processor: Partner with one that specializes in cross-border payments.

- Clearly communicate fees and conversions: Transparency reduces disputes.

- Secure transactions: Implement 3D Secure or AVS checks.

- Monitor transactions: Keep an eye on declines, chargebacks, and unusual patterns.

Why Understanding Cross-Border Payments Matters

Expanding globally increases revenue potential, but only if merchants understand the payment flow and pitfalls.

By learning how cross-border credit card payments work:

- You can reduce declines

- Avoid hidden fees

- Provide a better customer experience

- Build trust with international buyers